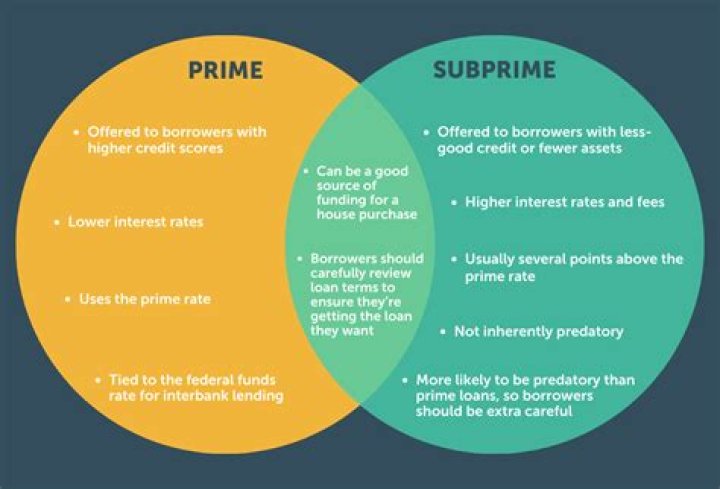

What is considered subprime

Subprime (credit scores of 580-619) Near-prime (credit scores of 620-659) Prime (credit scores of 660-719) Super-prime (credit scores of 720 or above)

What qualifies as subprime?

Experian defines subprime borrowers as those with a FICO® Score☉ in the fair range, between 580 and 669. FICO® Scores in this range are below average when compared with all U.S. consumers, and borrowers with fair scores are statistically more likely than the average borrower to fail to repay their creditors.

What are examples of subprime loans?

- Interest-Only Mortgages. Consider, for a moment, how a conventional mortgage works. …

- Dignity Mortgages. …

- Negative Amortization Loans. …

- Balloon Loans. …

- Adjustable Rate Mortgages (ARMs)

What interest rate is considered subprime?

A credit card for subprime borrowers can carry an interest rate of more than 25%, compared to less than 10% or even an introductory rate of 0% for a prime or superprime credit score.How do I know if my loan is subprime?

You might have a subprime loan if your mortgage has a much higher interest rate or a term longer than 30 years — or you had a down payment requirement higher than 20 percent (and you weren’t getting a jumbo loan or buying an investment property). Think back to the time when you applied for your mortgage, too.

Is Capital One a subprime?

Subprime credit cards are for people with bad or limited credit. Credit card companies may use specific credit score thresholds to define subprime. For example, Capital One, Chase and Citi define subprime as a credit score of 660 or below.

What makes someone a subprime borrower?

A subprime borrower is a person considered to be a relatively high credit risk for a lender. Subprime borrowers have lower credit scores and are likely to have multiple negative factors in their credit reports, such as delinquencies and account rejections.

What is considered a super-prime credit score?

For reference, Experian categorizes the five different borrower profiles into the following credit score ranges: Super-prime (781-850); Prime (661-780); Nonprime (601-660); Subprime (501-600); Deep subprime (300-500).Do subprime credit cards hurt your credit?

Some even charge inactivity fees. Subprime cards aren’t only more expensive than secured and prime cards, they can also hurt your credit utilization rating. … Not only is the card costing you more out of your pocket, it’s also potentially hurting your credit score. It’s easy to ruin your credit but hard to repair it.

Do subprime loans hurt your credit?A subprime loan, like any loan, can hurt your credit if you miss any payments or default on the debt. But it can also help improve your credit if you make your payments on time. … In contrast, a prime credit score is usually considered between 670 and 739, and a super-prime credit score 740 and above.

Article first time published onCan you still get a subprime mortgage?

Do subprime mortgages still exist? Mortgages for people with poor credit histories, or for people who don’t have significant deposits to put down on their properties, still exist – but they are now harder to find. They are also more expensive than standard mortgages.

What's the most common indicator of illegal property flipping?

The appraisal may include red flags symptomatic of inflated value. Many of the same red flags that accompany a traditional flip also apply to cash-out purchase fraud – straw buyer, false source of funds and false occupancy.

Is FHA a subprime loan?

Are FHA Loans Subprime Loans? FHA loans are not subprime loans. However, since FHA loans are available to borrowers with less than perfect credit or low-income, many look at them the same. FHA home loans are actually a great deal for homebuyers.

Why didn't people pay their mortgages in 2008?

Hedge funds, banks, and insurance companies caused the subprime mortgage crisis. … When the Federal Reserve raised the federal funds rate, it sent adjustable mortgage interest rates skyrocketing. As a result, home prices plummeted, and borrowers defaulted.

What is the difference between subprime and predatory lending?

Subprime lending is often considered to be predatory lending, which is the practice of giving borrowers loans with unreasonable rates and locking them into debt or increasing their likelihood of defaulting.

What is the difference between prime and subprime?

Prime borrowers are considered the least likely to default on a loan. Subprime borrowers, meanwhile, are viewed as higher default risks due to having limited or damaged credit histories. Lenders use several FICO® Score ranges to categorize loan applicants.

Is upgrade a subprime lender?

Indeed, the minimum credit score that a consumer need have to secure a loan from Upgrade, its minimum is 620, which the credit reporting bureau Experian says falls into the range of subprime borrowers who may be offered less-than-ideal loan terms because of their perceived ability to repay a loan on time.

How many people have a subprime credit score?

Only 11% of U.S. Consumers Have the Lowest FICO Scores More specifically, 11.1% of U.S. consumers have credit scores that are lower than 550. On a scale of 300–850, FICO scores that fall under the 580-threshold are considered to be very poor.

Why did I get charged interest on my credit card after I paid it off?

I paid off my entire bill when it was due last month and still got charged interest. … This means that if you have been carrying a balance, you will be charged interest – sometimes called “residual interest” – from the time your bill was sent to you until the time your payment is received by your card issuer.

Is Ollo card subprime?

Ollo is not a bank, as it does not offer other services, such as checking or savings accounts, CDs, or other products. Instead, Ollo is simply a credit card issuer, targeting those with “subprime” credit scores.

Is Discover subprime?

Although all of Discover’s credit card products are designed for consumers with fair or average credit and better, a subprime credit score is likely a bit too low for anything but the issuer’s secured product. Thankfully, it’s a great secured card.

What is considered a good credit score?

Generally speaking, a credit score is a three-digit number ranging from 300 to 850. … Although ranges vary depending on the credit scoring model, generally credit scores from 580 to 669 are considered fair; 670 to 739 are considered good; 740 to 799 are considered very good; and 800 and up are considered excellent.

Does Capital One do subprime auto loans?

A Capital One auto loan might be for you if you have a nonprime (between 601 and 660) or subprime (between 501 and 600) credit score. … Capital One works with borrowers with credit scores as low as 500.

What are some alternatives to using credit?

- Loan From Friends or Family. Consider asking folks close to you for a free or low-interest short-term loan. …

- 401(k) Loan. …

- Roth IRA. …

- Bank Personal Loan. …

- Collateral Loan. …

- Salary Advance. …

- Peer-to-Peer Loan. …

- Payday or Title Loan.

What is the minimum credit score for prime lending?

Mortgage loan products at PrimeLending Conventional loans from PrimeLending require a minimum credit score of 620.

What is interest rate will you pay with a deep subprime 300 500 credit score?

Credit Tier (Credit Score)Average New Car Loan Interest RateAverage Used Car Loan Interest RatePrime (661-780)3.64%5.35%Nonprime (601-660)6.32%9.77%Subprime (501-600)9.92%15.91%Deep subprime (300-500)12.99%19.85%

Can you have a credit score of 900?

A credit score of 900 is either not possible or not very relevant. … On the standard 300-850 range used by FICO and VantageScore, a credit score of 800+ is considered “perfect.” That’s because higher scores won’t really save you any money.

Can I buy a car with a 619 credit score?

A 619 FICO® Score is considered “Fair”. Mortgage, auto, and personal loans are somewhat difficult to get with a 619 Credit Score. Lenders normally don’t do business with borrowers that have fair credit because it’s too risky.

What does upside down on a loan mean?

Being upside-down on your car loan simply means you owe more than the car is worth. It’s sometimes called being underwater on the loan. So, if your car’s worth $10,000 but your loan balance is $12,000, then you’re $2,000 upside-down.

Which category of subprime loans do we consider the riskiest category for a lender?

The credit score of a deep subprime borrower Banks and lenders consider consumers who fall into the deep subprime category to be high risk, with a greater likelihood of defaulting on their payments. For this reason, deep subprime consumers have a hard time getting credit and, if they do, it comes at a high cost.

Do ninja loans still exist?

NINJA loans largely disappeared after the U.S. government issued new regulations to improve standard lending practices after the 2008 financial crisis. Some NINJA loans offer attractive low interest rates that increase over time.